New Europe Awakens: A Fresh Look at Post-Brexit Treasury

Published: June 15, 2020

Despite the challenges, the UK’s departure from the EU is an opportunity for corporates on both sides of the channel to re-engineer treasury workflows, overhaul legacy processes, and revamp treasury models. Andrés Baltar, Head of Europe, Corporate Banking at Barclays and Daniela Eder, Head of Payments & Cash Management Europe, Barclays, share up-to-the-minute insights on best practice treasury post-Brexit and outline how leading corporates are positioning their organisations for growth in the 'new Europe'.

Turn back the clock to 2016 – the year that music legends David Bowie and Prince passed away and Donald Trump became president of the United States. On 23rd June that same year, the UK voted to leave the European Union. Brexit negotiations swiftly became the order of the day for politicians, and corporates began planning for all potential exit scenarios.

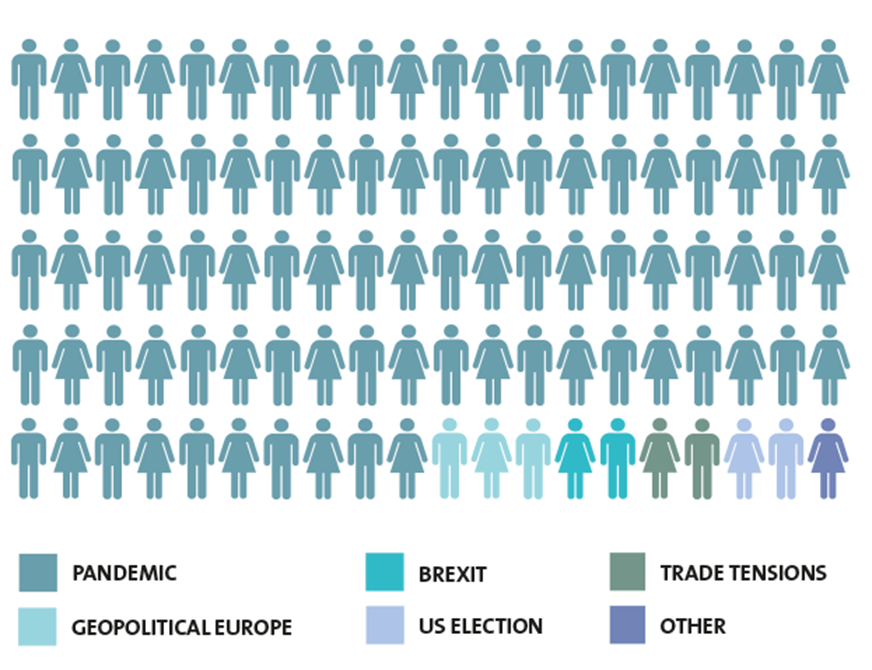

Fast forward to 2020, and the UK has now officially left the EU, but is in a transition period until the end of the year. Critically, however, no Brexit ‘deal’ has yet been reached and ongoing negotiations have been overshadowed by the global Covid-19 pandemic (see figure 1). Baltar comments: “Corporate treasurers’ attention has been diverted away from Brexit by the immediate need to focus on cash and liquidity as a result of the coronavirus crisis. This is understandable, but given the treasurer’s risk management responsibilities, Brexit must also remain firmly on the radar.”

Fig 1: Respondents’ number one geopolitical concern for 2020Source: TMI and Barclays research report: ‘New Europe: Is Your Treasury Fit for the Challenge?’

In fact, Baltar believes it is time to revisit Brexit plans that were formulated in the wake of the referendum four years ago, and to refresh them for the current environment. “Much has moved on since 2016,” he notes. “While uncertainty remains, the opportunities that Brexit presents are becoming clearer and leading companies are making the most of the momentum. Treasury digitisation has also accelerated, which is helping corporates to put in place an optimal cash management set-up – one that is flexible enough to change with the shifting operating environment.”

Connecting you to Europe

Barclays’ new European platform provides quick, consistent support for global corporates’ European banking – speeding up day-to-day tasks, so treasurers can focus on the bigger picture.

Unified across Europe, this platform offers harmonised transaction and reporting formats, together with standardised pricing and servicing models. Standard and regional electronic channels are supported across nine countries: Belgium; France; Germany; Ireland; Luxembourg; Netherlands; Portugal; Spain; and the UK.

In addition, electronic Know Your Customer (KYC) processes can be performed across all of these countries, removing the manual burden for clients.

This assertion is confirmed by a new research report published by TMI in partnership with Barclays, which surveyed 300+ treasury professionals and CFOs on current European treasury challenges and opportunities. According to the report, entitled New Europe: Is Your Treasury Fit for the Challenge?, 18% of respondents have used the momentum of Brexit to re-engineer treasury workflows, while 19% have benefitted from greater scrutiny over counterparties, given the need to review business relationships.

“It might seem counterintuitive, but now is the perfect time to step back and take a fresh look at your treasury operations. The twin forces of the Covid-19 pandemic and Brexit are empowering treasurers to look for greater efficiencies in their operations and deploy digital tools to help future-proof the department. That’s a rare mandate – and an opportunity that should not be missed,” Baltar comments.

But what exactly are leading corporates doing to prepare for Brexit? And where might efficiencies be found?

Making the move

“By and large, clients have approached Brexit in a very organised fashion – breaking down the potential impact on treasury into ‘buckets’ such as: liquidity, payment access, banking partners, location of operations and legal entity status, for example,” says Eder. “Initially, one of the major concerns for corporates and banks alike was the potential loss of passporting rights. This led organisations to review the location of their operations, with some choosing to create new European hubs. Banks were particularly fast movers here, and Barclays is no exception, with the expansion of Barclays Europe in Dublin. Many large corporates have also reviewed their European operations, but as the survey results show, some are still contemplating their options [see figure 2].”

Fig 2: Respondents considering moving UK treasury operations to Europe

Source: TMI and Barclays research report: ‘New Europe: Is Your Treasury Fit for the Challenge?’

Indeed, one in ten respondents with treasury operations in the UK are either considering moving them to elsewhere in Europe, or are in the process of doing so. “Some corporates are shifting treasury operations away from the UK to locations such as Ireland, the Netherlands and Luxembourg, to ensure they can carry on business as usual, regardless of the outcome of Brexit,” observes Baltar. “But there are also strategic opportunities within such moves, ranging from more advantageous tax regimes to innovation and optimisation incentives.”

“At Barclays, we see Brexit as an opportunity to serve our clients in the UK and the rest of Europe even more seamlessly. Alongside the expansion of our European base, we have invested in a new, streamlined European platform for clients. The user-friendly platform delivers a standardised client experience across Western Europe, and that consistency is precisely what corporates from the UK, US and Asia have been requesting. Europe is a key trading partner for them, and they are looking for a bank that has a presence across the region in order to facilitate optimal cash management.”

Interestingly, 35% of survey respondents are reviewing the location of their bank accounts to prepare for the ‘new Europe’. Baltar elaborates: “Access to European payments systems is critical, and this is one of the main drivers behind corporates moving bank account locations. There were long discussions around whether or not the UK would remain part of the Single Euro Payments Area (SEPA), which understandably made many corporates nervous – so some acted early and made the move.

“Nevertheless, the European Payments Council has now agreed that the UK will remain part of the SEPA scheme [1]. Corporates with euro accounts in the UK can also access TARGET 2 for high value payments via their banking partners – Barclays, for example, routes these payments through our Frankfurt office.”

Seeking out efficiencies

Some cutting-edge treasuries are also considering the use of virtual bank accounts instead of physical ones as they constantly review their bank account structures and efficiency. According to Eder, “While virtual accounts have long been used to create efficiencies in the receivables space, they are now being used in the form of virtual ledgers to enable corporates to replace physical bank accounts and easily set up an in-house bank offering payments-on-behalf-of [POBO] and receivables-on-behalf-of [ROBO].”

For those unfamiliar with the terminology, a virtual account management solution enables the sub-division of a physical bank account into numerous notional ‘virtual’ accounts. These virtual accounts function exactly the same way as a physical bank account – but have virtual IBANs. “At Barclays, new virtual accounts will in the future be opened or closed through a self-service portal, empowering treasurers to optimise their account structures at the click of a button,” says Eder.

Alongside virtual accounts, cash pooling is also in the spotlight. Baltar notes: “Just over a fifth [21%] of survey respondents are looking to review their cash pooling, which is prudent given both Brexit and the Covid-19 crisis. As the world has been reminded, liquidity is key to the survival of companies, and treasurers will increasingly be expected to update the board with accurate forecasts and even intra-day balances.

Fig 3: Treasury changes being made as a result of Brexit

Source: TMI and Barclays research report: ‘New Europe: Is Your Treasury Fit for the Challenge?’

“Moreover, cash pooling should be a journey of continuous improvement. Setting up a cash pool is only half the work – it ought to be regularly reviewed to ensure it is operating in an optimal manner and accurately reflects the changing needs of the business. Now is the opportune time to perform this kind of ‘stock take’. ”

Finally, Brexit could also be an opportunity to review and improve supply chain partnerships (12% of respondents agreed), as well as the financing of the company’s supply chain ecosystem, believes Baltar. “Supply chains are dynamic, so the way the supply chain is financed should be dynamic too. Treasurers should be asking questions of themselves and their banking partners: are the best working capital solutions being deployed, or are there more efficient solutions available? Could cards have a role to play alongside a supply chain finance programme, for example?”

Eder adds: “As risk managers, it is incumbent upon treasurers to ensure that the company’s treasury structure, and all of the areas treasury controls or influences, including supply chain finance, are fit for purpose. This means keeping a close eye on Brexit negotiations, even at a time when the world’s focus is elsewhere.”

Baltar echoes this, saying: “While the pandemic will likely dominate discussions in the months ahead, it is important that treasurers re-engage with the realities of Brexit.” In practical terms, this means dusting off Brexit preparation plans from several years ago and refreshing them to reflect any regulatory, tax, and/or operational changes. “Re-igniting dialogue with banking partners should also assist treasurers to see the bigger Brexit picture by examining the relative ‘fitness’ of the company’s cash management arrangements, as well as pinpointing potential efficiency opportunities,” he concludes.

About Barclays

Across Europe, Barclays can provide corporate banking services supported by deep local market knowledge. Barclays is supporting the European needs of global corporates with:

A unified banking platform across Europe

Harmonised transaction and reporting formats

Standardised pricing and servicing models across Europe

Support across standard and regional electronic channels

Barclays offers a range of cross-border services to support the success and growth of global corporates, by providing lending, risk management, cash and liquidity management, trade finance and sales financing. To find out more, visit barclayscorporate.com/europe

Source: TMI and Barclays research report: ‘New Europe: Is Your Treasury Fit for the Challenge?’

Source: TMI and Barclays research report: ‘New Europe: Is Your Treasury Fit for the Challenge?’